What Documents Should You Keep After Buying a Home?

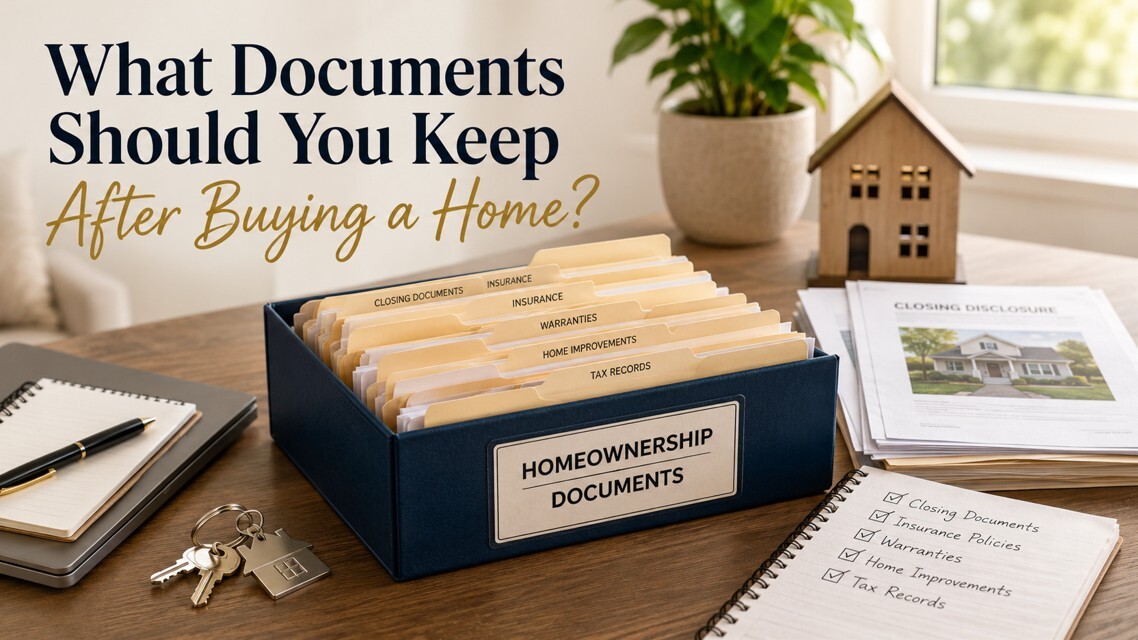

Buying a home comes with a significant amount of paperwork, and once the excitement of closing day has passed, it can be tempting to file everything away without another thought. However, keeping the right documents organized can save time, reduce stress, and protect your investment if questions or unexpected situations arise in the future.

Buying a home comes with a significant amount of paperwork, and once the excitement of closing day has passed, it can be tempting to file everything away without another thought. However, keeping the right documents organized can save time, reduce stress, and protect your investment if questions or unexpected situations arise in the future.

Keep Your Closing Documents

Your closing package contains important records that document the purchase of your home. This includes the Closing Disclosure, settlement statement, promissory note, deed, and mortgage documents. These records provide proof of ownership, outline the terms of your loan, and may be needed if you refinance, sell your home, or resolve a title issue.

Save Insurance and Warranty Information

Keep copies of your homeowners insurance policy and any updates or renewal notices. If your home came with builder warranties, appliance warranties, or a home warranty plan, store those documents together in an easily accessible location. Having these records available can make filing claims much easier.

Organize Home Improvement Records

Any major repairs, renovations, or upgrades should be documented with receipts, contracts, permits, and before-and-after photos. These records may help support insurance claims, provide documentation for future buyers, and potentially reduce taxable gains when you eventually sell your home.

Store Everything Securely

Many homeowners choose to keep digital copies in a secure cloud storage service while also maintaining physical copies of essential documents in a fireproof safe. Having both versions ensures your records remain available if something happens to the originals.

A little organization today can prevent frustration years from now. By keeping your most important homeownership documents together and updated, you will be better prepared for refinancing, insurance claims, tax questions, and eventually selling your home.

Buying a home is one of the biggest financial investments most people will ever make but protecting that investment is just as important. Homeowners insurance is often viewed as another monthly bill, yet the coverage you choose can have a significant impact on both your budget and your financial security. Understanding your options can help you balance affordability with the protection your home deserves.

Buying a home is one of the biggest financial investments most people will ever make but protecting that investment is just as important. Homeowners insurance is often viewed as another monthly bill, yet the coverage you choose can have a significant impact on both your budget and your financial security. Understanding your options can help you balance affordability with the protection your home deserves. Many people believe they need a large down payment before they can buy a home. While making a larger down payment can have benefits, it is not the only path to homeownership. Today’s mortgage programs offer a variety of options that allow qualified buyers to purchase a home with much less money upfront than they may expect. Understanding these opportunities can help turn the dream of owning a home into a reality sooner than you think.

Many people believe they need a large down payment before they can buy a home. While making a larger down payment can have benefits, it is not the only path to homeownership. Today’s mortgage programs offer a variety of options that allow qualified buyers to purchase a home with much less money upfront than they may expect. Understanding these opportunities can help turn the dream of owning a home into a reality sooner than you think.