Why Annual Mortgage Checkups Are a Smart Financial Habit

Your mortgage is one of the largest financial commitments you will ever make, yet many homeowners rarely review it after closing. Just as annual physicals help you stay healthy, an annual mortgage checkup can help ensure your loan, insurance, taxes, and financial goals remain aligned. Spending a few minutes reviewing your mortgage each year can uncover opportunities to save money and avoid costly surprises.

Your mortgage is one of the largest financial commitments you will ever make, yet many homeowners rarely review it after closing. Just as annual physicals help you stay healthy, an annual mortgage checkup can help ensure your loan, insurance, taxes, and financial goals remain aligned. Spending a few minutes reviewing your mortgage each year can uncover opportunities to save money and avoid costly surprises.

Review Your Interest Rate

Mortgage rates change over time, and so do your financial goals. While refinancing is not the right choice for everyone, reviewing current market conditions can help you determine whether opportunities exist to lower your monthly payment, shorten your loan term, or access equity responsibly.

Check Your Escrow Account

Property taxes and homeowners insurance premiums often change from year to year. Reviewing your escrow statement helps you understand why your monthly payment may have increased or decreased and gives you time to prepare for adjustments before they affect your budget.

Evaluate Your Home Equity

As you make mortgage payments and home values change, your equity grows. Understanding how much equity you have can help you plan for future renovations, debt consolidation, or other financial goals. It also allows you to track the progress you are making toward full ownership.

Update Your Financial Goals

Life changes quickly. A new job, growing family, retirement planning, or paying off other debt may influence how your mortgage fits into your overall financial picture. An annual review is a good opportunity to make sure your home financing continues to support your long-term goals.

A mortgage should not be something you think about only when you buy or sell a home. A simple yearly review helps you stay informed, identify opportunities, and make confident financial decisions throughout your homeownership journey.

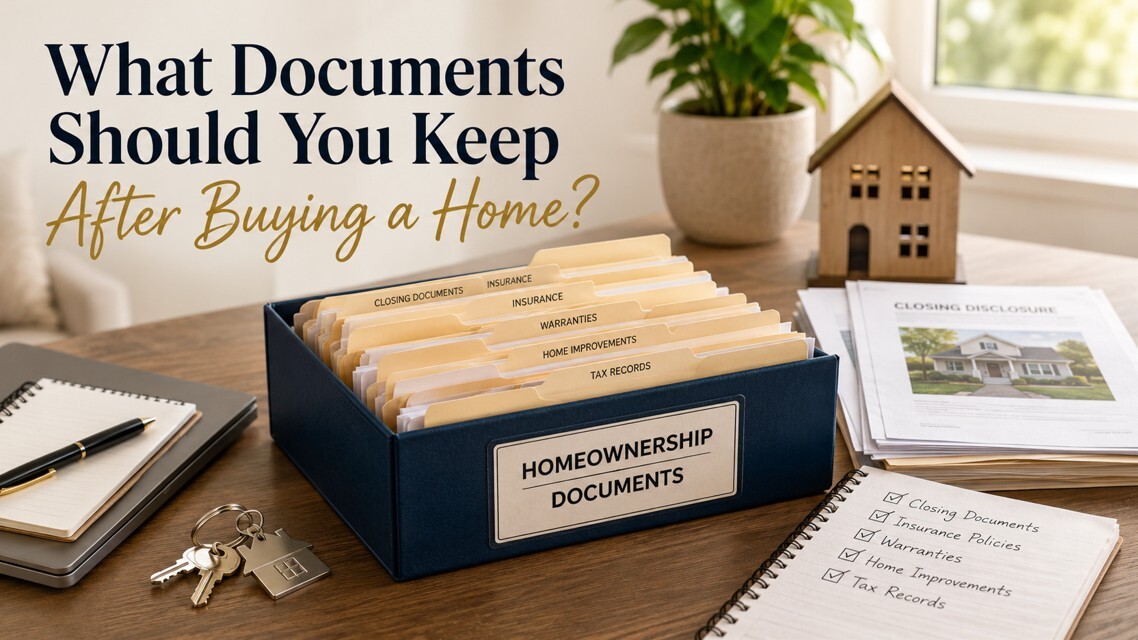

Buying a home comes with a significant amount of paperwork, and once the excitement of closing day has passed, it can be tempting to file everything away without another thought. However, keeping the right documents organized can save time, reduce stress, and protect your investment if questions or unexpected situations arise in the future.

Buying a home comes with a significant amount of paperwork, and once the excitement of closing day has passed, it can be tempting to file everything away without another thought. However, keeping the right documents organized can save time, reduce stress, and protect your investment if questions or unexpected situations arise in the future. Buying a home is one of the biggest financial investments most people will ever make but protecting that investment is just as important. Homeowners insurance is often viewed as another monthly bill, yet the coverage you choose can have a significant impact on both your budget and your financial security. Understanding your options can help you balance affordability with the protection your home deserves.

Buying a home is one of the biggest financial investments most people will ever make but protecting that investment is just as important. Homeowners insurance is often viewed as another monthly bill, yet the coverage you choose can have a significant impact on both your budget and your financial security. Understanding your options can help you balance affordability with the protection your home deserves.